Home Equity Loans Bc for Beginners

Table of ContentsExcitement About Mortgages VancouverMortgages Vancouver Can Be Fun For EveryoneSome Ideas on Home Equity Loan Vancouver You Need To KnowLittle Known Questions About Loans Vancouver.The 7-Minute Rule for Home Equity Loans VancouverMore About Home Equity Loans Bc

Still have inquiries? Right here are a few other concerns we have actually addressed:.In a house equity loan, you can borrow a lump amount of money that you typically settle in fixed installations over a regard to five to thirty years. Just how much you can obtain will rely on how much of your home you have outright. Pros and disadvantages of a house equity loan Here are some benefits and drawbacks to consider before you start completing lending paperwork.

It won't raise, even when the Federal Reserve raises rates of interest. Using genuine estate as collateral usually garners lower rates of interest contrasted to other types of lendings. Since you're borrowing one round figure and also have a fixed interest price, your settlements are foreseeable as well as won't differ over the life of the financing.

Little Known Questions About Second Mortgage Vancouver.

If you pick to utilize your house equity funding proceeds to boost your residence, you may be able to deduct the rate of interest from your taxed income - Loans Vancouver. Cons Because a house equity finance's rate of interest won't fluctuate with the market, unlike a house equity credit line (HELOC), the price for a home equity financing is commonly higher.

Just like the majority of finances entailing property, you'll probably have to pay closing costs. These prices can vary from 2% to 5% of the finance quantity. If you still have a primary mortgage, you currently have 2 home loan settlements, which can reduce your non reusable income as well as make your regular monthly spending plan tighter. Mortgages Vancouver.

Several lenders have rigorous home equity financing requirements, such as greater credit rating minimums and less flexibility for higher debt-to-income (DTI) proportions. Differences between HELOCs as well as residence equity lendings Several things are set in rock with a home equity finance, such as your rate of interest. In a HELOC, nevertheless, several variables can transform in time.

What Does Home Equity Loans Vancouver Mean?

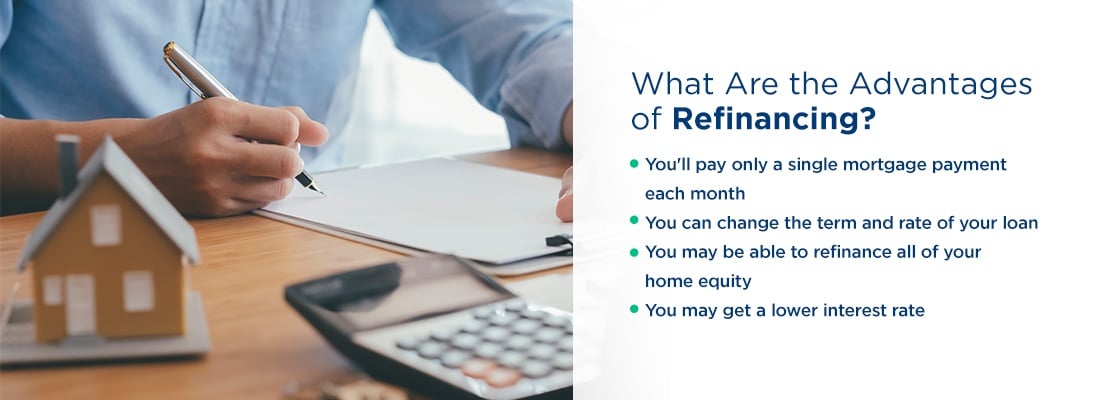

3 options to a house equity lending Cash-out re-finance A cash-out refinance can be an effective economic tool, providing you accessibility to the equity in your home without producing a bank loan payment. When you refinance into a cash-out finance, you obtain greater than you need to mortgage your house as well as pocket the difference in cash money.

If you extend your lending term, you could pay more in interest over the life of the funding. HELOCs have an established draw duration, such as 10 years.

The Ultimate Guide To Home Equity Loan Vancouver

Due to the fact that personal lendings aren't protected they only rely on your credit rating their rates of interest have a tendency to be more than finances with security, such as a residence or automobile. The typical individual finance rate of interest for borrowers with exceptional credit rating (760-plus) is around 9%, according to Financing, Tree data.

You've possibly heard of home equity lendings as well as residence equity credit lines (HELOCs) - but just how valuable are they when it involves funding improvements? You can use a residence equity loan or HELOC for bathroom and kitchen remodels, landscape design, new roof as well as house siding, as well as more. Typically property owners make use of HELOCs to fund significant remodelling jobs, as the rate of interest are less than they are on personal lendings and charge card.

In this overview, we are mosting likely to take an appearance at what house equity you can check here financings and also HELOCs are, just how they work for financing remodellings, just how much you can borrow, and the advantages and disadvantages to both of these options. A conventional HELOC could not be the very best method for you to fund your improvement.

Some Known Facts About Home Equity Loans Bc.

Making Use Of Equity To Finance Residence Improvements, Utilizing equity to fund a residence restoration job can be a smart move. You require to understand just how it works to be able to figure out your ideal financing option. The larger the difference between the amount you owe on your mortgage and the worth of your house, the extra equity you have actually obtained.

Yet your residence's value can drop, as well as up. Home costs alter consistently, and also when the marketplace is executing well and also prices get on the surge, your equity will enhance. However when the marketplace is down, this can reduce see the value of your home and minimize your equity.

As an example, if your residence deserves $500k and your existing home loan balance is $375k, a residence equity lending might let you borrow as much as $75k. (90% multiplied by $500k, minus $375k)These are guaranteed loans that utilize your house as collateral, meaning this that you might lose this in case you are unable to pay.

How Loans Vancouver can Save You Time, Stress, and Money.

House improvement projects are one of the most usual objective, however, with the United States Demographics Bureau's Housing Study confirming that approximately 50% of home equity finances are made use of in this way - Foreclosure Loans. They're generally fixed-rate finances with established terms, payments, and routines. Once you're approved for a financing, you get the total in one swelling sum.

Tapping all the equity in your house in one swoop can work versus you if home worths in your location decline. If property values decrease, the market value of your home might decline, and you could finish up owing even more than your residence is worth. The house could be marketed to please the remaining financial obligation if the finance is not repaid or enters into default.